Mortgage recasting is an easy way to reduce your monthly mortgage payments without the hassle of refinancing. By making a lump-sum payment toward your loan balance, you can have your lender adjust your monthly payments while keeping the same interest rate and loan terms. It’s a straightforward and cost-effective way to ease financial pressure and improve cash flow, whether you’re a homeowner, investor, or real estate professional.

Table of Contents

ToggleWhat is a Mortgage Recast?

A mortgage recast is a process where the lender recalculates your monthly payments based on your current loan balance after you make a substantial lump-sum payment. Unlike refinancing, a recast doesn’t involve changing your interest rate or loan term—it simply lowers your monthly payment by reducing the principal balance.

Key Features of Mortgage Recasting

- No Need to Refinance: Avoid refinancing hassles and closing costs.

- Lower Monthly Payments: Payments are recalculated to reflect the reduced loan balance.

- Same Interest Rate: Your original loan terms remain unchanged.

- Cost-Effective: A small administrative fee (typically $150-$500) is charged instead of expensive closing costs.

How Does a Mortgage Recast Work?

Mortgage recasting is a simple process that can lower your monthly payments. First, you make a large lump-sum payment toward your mortgage principal, reducing the loan balance. Then, you contact your lender to request a recast. The lender recalculates your monthly payment based on the new balance, while your interest rates and loan term stay the same.

For example, if you have a $300,000 mortgage at 4% interest with a monthly payment of $1,432, and you make a $50,000 lump-sum payment, your new loan balance becomes $250,000, and your recalculated monthly payment drops to $1,194.

💡 Pro Tip: The larger your lump-sum payment, the more significant the reduction in your monthly payments.

Who Benefits from a Mortgage Recast?

First-Time Homebuyers

- Great option if you’ve come into extra funds, like a bonus or inheritance.

- Helps ease monthly financial strain.

Seasoned Investors

- Ideal for maintaining liquidity while managing multiple properties.

- Keeps your cash flow intact without altering your investment strategy.

Real Estate Professionals

- Recasting offers a valuable solution for clients who want flexibility without refinancing.

- Demonstrates your expertise by recommending cost-saving strategies.

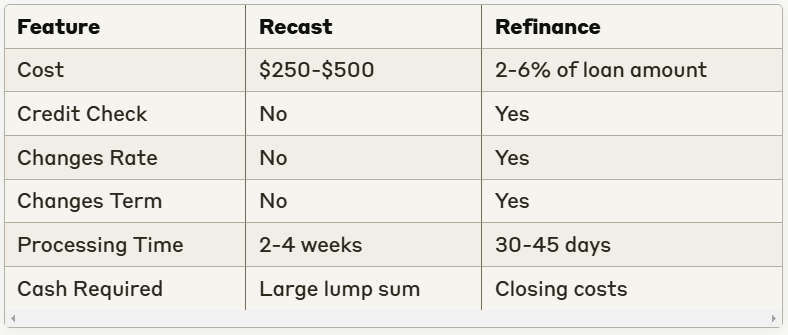

Recast vs. Refinance

Steps to Get Started with Mortgage Recasting

- Check Eligibility: Not all loans qualify for recasting. Most conventional loans do, but FHA and VA loans typically don’t.

- Plan Your Lump-Sum Payment: Ensure the payment significantly reduces your loan balance.

- Contact Your Lender: Request details about their recasting process, fees, and timelines.

- Complete the Process: Pay the required fee, and your lender will recalculate your payment.

Advantages and Disadvantages of Mortgage Recasting

Pros

✅Lower Monthly Payments: Easier to manage household budgets.

✅Minimal Fees: A fraction of refinancing costs.

✅Keeps Loan Terms Intact: No changes to the interest rate or loan length.

Cons

❌ Lump-Sum Requirement: Requires access to extra cash.

❌ No Interest Rate Reduction: Doesn’t help if current rates are lower than yours.

❌Not Available for All Loans: FHA and VA loans are usually excluded.

Practical Tips for Recasting Success

- Use a Lump-Sum Windfall: Bonuses, inheritances, or tax refunds can fund the payment.

- Maintain an Emergency Fund: Don’t deplete savings to recast.

- Run the Numbers: Use online mortgage recasting calculators to estimate your savings

Is Mortgage Recasting Right for You?

Mortgage recasting is a powerful tool for reducing monthly payments without the complexity of refinancing. It’s especially useful for those with extra cash to apply toward their principal while keeping their interest rate intact.

For first-time buyers, it provides breathing room; for investors, it optimizes cash flow; and for real estate professionals, it’s a practical solution to share with clients. Explore potential savings or consult with a trusted real estate professional for personalized advice.