Mortgage pre-approval is a crucial step in the home-buying process that can significantly influence your purchasing power and overall experience. Understanding the distinction between mortgage pre-approval and pre-qualification is essential for any prospective homebuyer. While both terms are often used interchangeably, they represent different stages in securing a mortgage and can have varying impacts on your ability to make competitive offers on homes. In this blog, we will explore the key differences between mortgage pre-approval and pre-qualification, helping you make informed decisions as you embark on your journey to homeownership.

Mortgage Pre-Approval

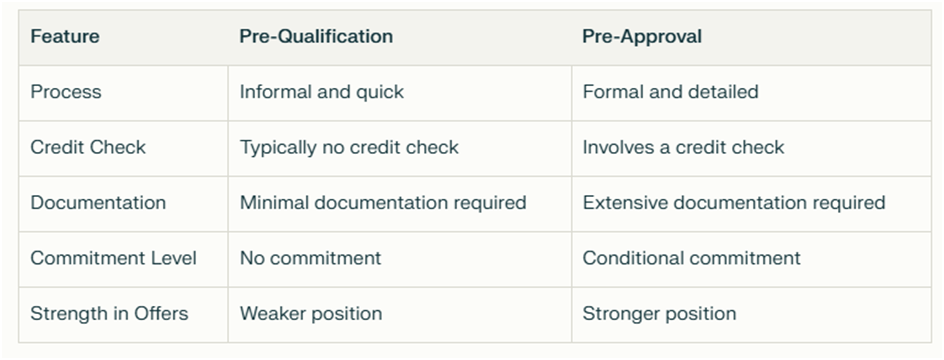

Mortgage pre-approval is a more formal and detailed process than pre-qualification. It involves a thorough evaluation of your financial situation by a lender, providing you with a conditional commitment for a specific loan amount.

Process

- Detailed Application: You complete a formal application and provide documentation such as pay stubs, tax returns, and bank statements.

- Hard Credit Check: The lender conducts a hard credit check to assess your creditworthiness.

- Conditional Approval: If approved, you receive a pre-approval letter indicating the amount you can borrow under specific conditions.

Benefits

- Stronger Position: A pre-approval letter demonstrates to sellers that you are a serious buyer with verified financial backing.

- Accurate Budgeting: It provides a clearer picture of what you can afford, allowing for more focused home searches.

- Faster Closing Process: Much of the paperwork is completed upfront, potentially speeding up the closing process once you find a home.

Mortgage Pre-Qualification

Mortgage pre-qualification is the initial step in the mortgage process. It involves providing a lender with basic financial information, such as your income, debts, and assets. Based on this preliminary data, the lender gives you an estimate of how much you might be able to borrow.

Process

- Information Submission: You share your financial details with the lender.

- Quick Assessment: The lender evaluates this information and provides an estimated loan amount.

- Soft Credit Check: Typically, this process involves a soft credit check, which does not impact your credit score.

Benefits

- Speed: Pre-qualification can often be completed quickly, sometimes within minutes.

- Budgeting Tool: It helps you understand your potential budget when house hunting.

- No Commitment: Since it’s an informal estimate, there’s no obligation to proceed with that lender.

Key Differences Between Pre-Approval and Pre-Qualification

When to Use Each Option

Pre-Qualification

Consider getting pre-qualified at the start of your home-buying journey. It’s an excellent way to gauge how much you might be able to borrow without impacting your credit score. This step allows you to feel confident when browsing homes within your price range.

Pre-Approval

Once you’ve defined your budget and are ready to make offers on homes, obtaining a pre-approval is advisable. It strengthens your position in negotiations and shows sellers that you have the financial means to follow through on an offer.

Pro Tips

- Don’t confuse these terms – they’re not interchangeable

- Always aim for pre-approval before house hunting

- Keep your financial situation stable during the pre-approval process

- Be prepared to provide detailed financial information

- Shop around and compare pre-approval offers from multiple lenders

Final Thoughts

While pre-qualification can help you understand your potential borrowing range, pre-approval is the gold standard when you’re serious about buying a home. It provides clarity, credibility, and confidence in your home-buying journey.

Remember: Understanding the nuances between pre-qualification and pre-approval can make your path to homeownership smoother and more strategic.