For eligible homebuyers and sellers, VA loan assumption is a powerful financial tool that can simplify the homeownership process. This strategy allows a new buyer to take over an existing VA loan, often at more favorable terms than what’s available in the current market. However, while the concept may sound appealing, it comes with its own set of costs, fees, and strategic considerations.

In this guide, we’ll explore the ins and outs of VA loan assumption, breaking down its financial implications and offering insights to help you make informed decisions. Whether you’re a seller looking to attract buyers or a buyer seeking lower interest rates, understanding the nuances of this process is key to maximizing its benefits

Table of Contents

ToggleWhat is VA Loan Assumption?

VA loan assumption is a specialized process that enables a qualified buyer to take over an existing VA loan from the current homeowner. Instead of refinancing or securing a new loan, the buyer adopts the original loan’s terms. This approach can offer significant benefits, such as inheriting a lower interest rate and bypassing the more complex steps typically associated with traditional mortgage financing.

Key Features:

- Exclusively applies to VA loans

- Requires approval from the VA

- Transfers loan repayment responsibility to the buyer

- Offers potential for significant cost savings

Breakdown of VA Loan Assumption Fees

When assuming a VA loan, there are a few key fees to consider. Here’s a simple explanation of the potential costs:

VA Funding Fee:

- A one-time fee, usually 0.5% of the remaining loan balance for first-time assumptions.

- Example: For a $300,000 loan, this would be about $1,500.

Credit Report and Processing Fees:

- Credit check: $30–$50.

- Loan processing fees: Typically $300–$800, depending on the lender.

- Additional administrative costs may also apply.

Appraisal Costs:

- A VA appraisal, required to confirm the property’s value, usually costs $300–$700.

Legal and Title Transfer Expenses:

- Title search fees range from $200–$400.

- Legal documentation and title transfer can cost $500–$1,000.

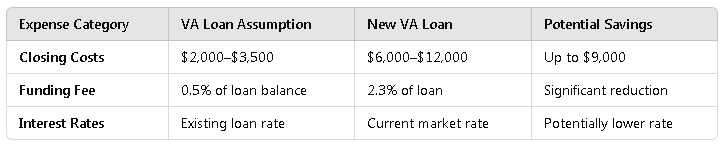

Cost Comparison: Assumption vs. New Loan

Here’s a simple breakdown of how the costs differ between assuming a VA loan and taking out a new one:

VA loan assumptions often provide significant cost savings, especially with lower funding fees and the ability to keep the existing loan’s interest rate, which could be lower than current market rates.

Potential Savings and Financial Considerations

Taking over a VA loan can offer some great financial benefits but also comes with certain challenges. Here’s a simple breakdown:

Advantages

- Lower Closing Costs: Assumptions often cost much less than starting a new loan.

- Potentially Lower Interest Rates: You can inherit the original loan’s interest rate, which might be better than current rates.

- Faster Loan Processing: The process is typically quicker than applying for a new loan.

- Reduced Paperwork: Less documentation is needed compared to a traditional mortgage.

Potential Drawbacks

- Strict Qualification Requirements: The buyer must meet VA standards to take over the loan.

- Limited Availability: Not all loans or properties are eligible for assumption.

- Potential Assumption Constraints: Some lenders or loan terms may impose additional conditions or fees.

Step-by-Step Guide to VA Loan Assumption

1.Verify Assumability

- Check if the current VA loan can be assumed. Not all VA loans are eligible.

- Contact the current lender to confirm and get details on the process.

2. Qualification Process

- Ensure you meet VA’s credit and income requirements.

- Be ready for a credit check and provide necessary financial documents, such as proof of income.

3. Financial Evaluation

- Calculate how much you might save by assuming the loan compared to getting a new one.

- Compare the existing loan’s interest rate with current market rates.

- Think about the long-term financial impact, including monthly payments and fees.

The Bottom Line

VA loan assumption offers a unique opportunity for both buyers and sellers to benefit from lower costs, favorable interest rates, and streamlined processes. For buyers, it’s a chance to secure affordable financing by stepping into an existing loan’s terms. For sellers, it can be a valuable selling point in attracting qualified buyers. However, navigating the process requires careful consideration of fees, eligibility requirements, and financial implications.

By understanding the costs and steps involved, you can make an informed decision about whether a VA loan assumption aligns with your financial goals. Whether you’re looking to save on closing costs, take advantage of a lower interest rate, or simplify the home-buying process, this strategy can be a powerful tool when approached strategically.